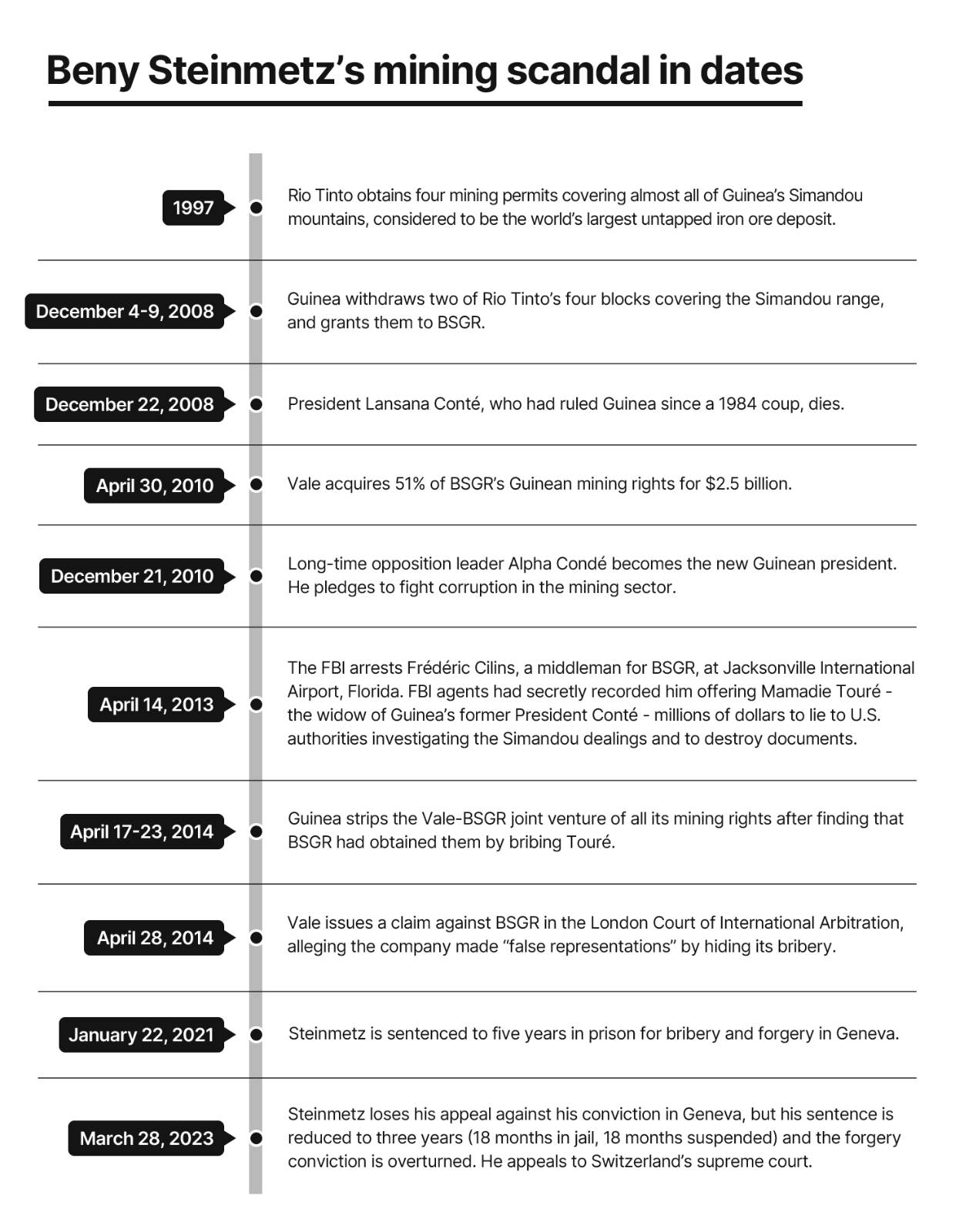

Mining magnate Beny Steinmetz has spent more than a decade tackling negative headlines, outwitting former business partners, and grappling with multiple investigations and lawsuits.

A wiry 68-year-old with a penchant for high-risk deals, Steinmetz has been arrested in three countries — most recently in Cyprus, where he spent nearly a month in jail fighting extradition towards the end of last year — before emerging triumphant.

His most significant legal troubles, however, have been in Switzerland. In 2021, a Geneva criminal court found that Steinmetz and his associates paid millions of dollars to the wife of Guinea’s president to obtain the mining rights to valuable iron ore deposits — half of which Steinmetz’s firm then quickly sold for billions in profit.

Steinmetz has denied all allegations of corruption, telling the Geneva court, “I’m innocent and I have nothing to reproach myself with.” He is appealing his conviction to Switzerland's supreme court after being given a three-year sentence.

Now, OCCRP can reveal how a Bahamas-registered company, called Global Special Opportunities Limited (GSOL), struck deals with Steinmetz’s companies as the businessman faced mounting pressure from the fallout of the Guinea bribery accusations. Reporters found that on at least five occasions, GSOL — or other firms controlled by its founder, Greek businessman Sabby Mionis — took actions that proved key to Steinmetz’s fight-back.

There is no suggestion or evidence that Mionis — or his companies or directors — did anything illegal. However, he did seize the opportunities presented as Steinmetz was seeking to escape the consequences of his alleged corruption. Both businessmen say the deals were at arm’s length and offered their own commercial explanations. The ultimate results are clear: they helped Steinmetz in his battles, as creditors and law enforcement came after him.

OCCRP has laid out the facts, and the complex strategies Steinmetz and his firms put in place after his mining scandal erupted.

The Steinmetz Scandals

OCCRP found Steinmetz and Mionis’s companies have done business together in North Macedonia, the U.S., and West Africa. In an interview with OCCRP, Mionis described his relationship with Steinmetz as “a friendship, like I have with many business people.”

Sabby Mionis during an interview at Israeli Television i24NEWS.

GSOL, which was set up in 2009, first invested in “hedge funds, in distressed debt, in litigation” and other areas, GSOL director Marcos Camhis told OCCRP in the same interview. During its first five years, the company kept a low public profile. “It was not something we had to advertise,” Camhis said.

The earliest available records of GSOL’s business activities are from 2015, when it made a bid to acquire a company related to Steinmetz. This was soon after Steinmetz started to face serious legal consequences for alleged corruption in Guinea. In April 2014, a new Guinean administration confiscated Steinmetz’s iron ore rights, after finding they had been obtained through bribery. The action triggered a wave of court cases from business rivals and former partners, and was accompanied by corruption investigations in several countries.

GSOL’s deals with Steinmetz’s companies helped it rise from obscurity to become a globally significant player in the mining and metals sectors.

OCCRP reporters used evidence from court cases, along with corporate documents and land registry filings, to uncover a paper trail of Mionis and GSOL’s ties to Steinmetz. They found multiple cases around the world in which their actions helped Steinmetz:

October 2015: After Beny Steinmetz Group Resources (BSGR) — the Israeli businessman’s flagship company — got into a dispute with its business partner in a North Macedonian nickel refinery, a company owned by two GSOL directors sent millions of dollars to BSGR in a failed attempt to take control of the plant. GSOL itself ended up acquiring the nickel refinery in 2019.

Late 2016 and early 2017: GSOL became the major creditor to Steinmetz’s diamond mine in Sierra Leone after buying $136 million of its debt from Standard Chartered bank and the U.S. luxury jeweler Tiffany & Co. Court filings suggest Steinmetz and BSGR eased the way for GSOL to buy the debt at a knockdown price, which also protected the mine from being seized by creditors.

November 2017: An offshore firm owned by GSOL’s founder Mionis financed a $20 billion lawsuit brought by BSGR in New York against the billionaire philanthropist George Soros. BSGR later described the expected proceeds of the lawsuit (which was eventually dismissed) as a major future asset, allowing it to avoid liquidation when it declared itself insolvent in early 2018.

November 2017: Another company owned by Mionis partnered with a U.S. firm to buy a Chicago skyscraper for $86.4 million. Mionis claims Steinmetz had no interests in the partner firm, but corporate documents obtained by OCCRP reveal that Steinmetz’s representatives played a central role in organizing the purchase and that he ended up owning a small stake.

February 2019: A GSOL subsidiary participated in discussions over a provisional settlement between Guinea and BSGR, which led to Guinea withdrawing as a plaintiff in the criminal prosecution of Steinmetz in Geneva. The provisional deal hinged on Steinmetz and GSOL partnering in a lucrative new mining venture.

Steinmetz said through a lawyer that he has “no control over GSOL and neither GSOL nor its affiliates are agents or nominees” of his. He said he “never had any interest, direct or indirect, in GSOL or any of its subsidiaries.” There is no suggestion that GSOL or its directors were proxies for Steinmetz or his companies.

Steinmetz has consistently denied the Guinea bribery allegations and has called his arrests politically motivated.

Lawyers for Mionis and Camhis said they “did not help ‘shield’ Mr. Steinmetz, or ‘fight his battles’ at any point. Their investment decisions were made based on the merits of each investment.”

GSOL’s lawyer said the company “does not and has not represented the interests of BSGR, Mr Steinmetz or any of their respective related parties.”

Steinmetz Enemy Pointed Finger at GSOL

Among Steinmetz’s adversaries, one looms large — Brazilian mining giant Vale S.A.

In 2010, Vale agreed to pay $2.5 billion for a 51-percent stake in the Guinean mining rights that Steinmetz’s BSGR had acquired. But, along with BSGR, it lost its share of the rights when the Guinean government took them back four years later.

Vale accused BSGR of having lied repeatedly about its alleged bribery, in order to secure the Brazilian mining firm's investment, and blamed it for huge losses. In 2019, Vale won a $2 billion award against BSGR at a business dispute tribunal, the London Court of International Arbitration, but BSGR said it was insolvent and couldn’t pay.

Vale has so far been unsuccessful in forcing BSGR to pay up the $2 billion it is owed, and court proceedings have seen no real movement for over a year.

As Vale battled in U.S. courts to force BSGR to pay up, the Brazilian firm’s lawyers claimed in court filings that companies tied to GSOL and Mionis were part of a scheme “that appears engineered to put assets out of the reach of BSGR’s creditors.”

Vale later rowed back some of its claims in an April 2023 joint statement, saying that documents it had subpoenaed from a Mionis company “did not provide any evidence” that Mionis, Camhis or their associates had acted as Steinmetz’s agents. Neither did the documents show that they “were involved with any effort by Mr Steinmetz or any Steinmetz entity to hide assets from creditors.”

Mionis has claimed this statement as exoneration, telling OCCRP it meant “Vale retracted everything.” In fact, the Vale statement only dealt with one part of its wider accusations, and only one set of documents.

October 2015: GSOL Directors’ Firm Funds Steinmetz Company

Steinmetz’s company and GSOL are first known to have been involved in common deals in what is now North Macedonia, where BSGR had been at odds with its partner in a major nickel ore producer.

FENI Industries A.D. had been one of the jewels of Yugoslavia’s mining industry before the country broke up in the early 1990s. BSGR acquired FENI in the mid-2000s, alongside International Mineral Resources (IMR), a mining company owned by the Central Asian billionaires Alexander Machkevitch, Patokh Chodiev, and Alijan Ibragimov, collectively known as the “Trio.”

But by 2015, the refinery was on the brink of bankruptcy. Relations between BSGR and IMR soured, and they fell into a boardroom dispute over FENI’s direction.

Then a Bahamas-registered company, Tower View Asset Management Ltd., appeared on the scene. The company — which is part-owned by Camhis and officially served as GSOL’s “investment adviser” — offered $150 million for FENI’s holding company, Cunico Resources N.V., in March 2015. But IMR rejected the offer.

Six months later, BSGR and IMR took their dispute to a mediation chamber in Amsterdam, where Cunico was registered. The mediators gave each of Cunico’s pre-existing shareholders — Steinmetz’s company or the Trio’s — the chance to buy new shares and become the majority owner of the company. For their bids to be considered, the companies each needed to make $5 million available within days.

Tower View Asset Management reappeared, providing the funds to BSGR.

Mionis and Camhis told OCCRP the funding for BSGR’s bid ultimately came from the GSOL group. “Our interest was to acquire the company, so any funding or discussion we had was to end up acquiring the company” from BSGR, said Camhis.

Despite these efforts, the Trio’s IMR emerged victorious from the bidding process and committed to inject tens of millions of dollars into Cunico. IMR and its parent company increased their share from 50 to around 90 percent, while BSGR’s share was reduced from 50 to around 10 percent.

But GSOL did not give up its pursuit of FENI, which continued to struggle under its new ownership structure.

FENI’s lenders filed a bankruptcy petition in October 2017. In early 2018, GSOL swooped in and began operating FENI before acquiring the plant outright in 2019.

Allegations of Conflict of Interest in Bankruptcy Process

North Macedonia’s deputy prime minister, Koco Angjushev, was involved in negotiations related to the FENI bankruptcy process, according to a lawsuit filed by BSGR’s former business partner. But Angjushev was also one of FENI’s key creditors, through his company, Energy Delivery Solutions S.A.

GSOL’s tenure at FENI — now renamed Euronickel — proved relatively short-lived. Amid a spike in electricity costs and reported disputes with suppliers, the company saw renewed financial difficulties. In December 2023 its biggest creditor, Komercijalna Banka, acquired the plant in a forced sale, before agreeing to sell it on to a Turkish conglomerate in March.

IMR did not reply to emailed questions.

Steinmetz’s lawyer did not directly address the question of GSOL’s funding of BSGR’s bid, but dismissed any suggestions of wrongdoing around the FENI case and the dispute with IMR as “baseless.”

September 2016: GSOL Becomes Steinmetz’s Top Diamond Creditor

While BSGR battled over its nickel interests in Macedonia, a bigger threat was circling over the company — its former partner, Vale.

Guinea had revoked BSGR and Vale’s jointly held mining licenses in April 2014, prompting Vale to launch its arbitration case against BSGR in London.

Steinmetz argued his company was blameless over the cancellation of the licenses, and that bribery allegations were based on “forged contracts.” But from August 2016, BSGR was on the back foot, refusing to show up for hearings and seeking to have all the arbitrators dismissed on grounds of bias.

If it lost, BSGR risked having to hand its assets to Vale as payment, including the most valuable of them all — the Koidu diamond mine in Sierra Leone.

Koidu, the largest diamond mine in Sierra Leone.

But even before the arbitration tribunal issued a ruling, a complex set of transactions led to GSOL acquiring rights over the mine. As a result, GSOL would now be first in line to seize the mine ahead of any other potential BSGR creditor, including Vale.

The arrangements involved GSOL buying up Koidu’s debts at a significant discount.

The debt purchase came about because, in mid-2015, Koidu’s parent company, Octea Ltd., had defaulted on repayments to its major lenders, Standard Chartered and the luxury jeweler Tiffany & Co. Under the terms of its funding agreement, Standard Chartered now had the right to seize the mine to recoup its loan.

But in September 2016, GSOL bought up $92 million of the mine’s debt from the bank, paying the cut-rate price of $14 million, and replaced the bank as Koidu’s top creditor, with rights over the mine as collateral.

Mionis told OCCRP he first got the idea of buying the debt “in my discussions with Steinmetz.”

“I realized there was a distressed situation there, and distresses always make me tick … So I said to Marcos [Camhis], ‘Look into it.’” Camhis said one of Steinmetz’s top executives, Dag Cramer, took him to his first meeting with Standard Chartered. Mionis and Camhis said that GSOL’s intervention saved Koidu from being seized by Standard Chartered.

But later court records raise questions over the commercial sense of the deal for BSGR, and whether BSGR and GSOL acted independently in the course of the transaction. They show BSGR committed to make a $16 million “settlement payment,” which would rise to $74.5 million if not paid on time, to Standard Chartered to exit the loan and ensure the deal went through, and that BSGR even may have financed GSOL’s debt purchase. (BSGR failed to make the settlement payment to Standard Chartered, according to the latest available information.)

Years after the debt deal was struck, both Standard Chartered and Vale raised concerns that GSOL and Steinmetz’s companies may have been acting in concert.

Koidu’s parent company Octea promised $15.3 million to GSOL ahead of the debt deal, and this was then paid out by a Steinmetz family company, according to Standard Chartered and Vale. This payment led Standard Chartered to say, in a letter to BSGR’s administrators, that the relationship between GSOL and the BSGR group of companies was “not a true third party arrangement.”

Lawyers for GSOL, Mionis, and Camhis told OCCRP there was “nothing improper” about the deal, and that their clients did not collude with BSGR on the debt dealings.

Steinmetz’s lawyer said the transactions “were entered in arm’s length terms” and that Steinmetz “is not involved in the management of Koidu,” as BSGR is under administration. He said Koidu “respects the best practices of the mining industry.”

Bank Raises Questions Over Debt Purchase

During the cross-examination of Steinmetz executive Dag Cramer in London, Vale’s lawyer cited documents that suggested a Steinmetz company may have financed GSOL’s purchase of the Koidu debt from Standard Chartered.

Standard Chartered would not comment on the debt dealings, citing its “duty of confidentiality,” while Tiffany’s did not respond to questions. There is no suggestion of wrongdoing against either of the former lenders. Cramer said he “was not involved in any of the discussions” the GSOL group had over the debt.

November 2017: Mionis Bankrolls Major Steinmetz Lawsuit Against Soros

As the Sierra Leone debt deals were being concluded, Steinmetz's troubles went from bad to worse over the Guinea bribery affair.

Prosecutors in Geneva had begun probing his role in the iron ore deal and in December 2016 he was briefly put under house arrest in Israel, where police were also investigating the matter. Israeli authorities ultimately released him without charge.

In April 2017, BSGR filed a lawsuit against George Soros in New York, which deflected attention from Steinmetz’s alleged role in the Guinea bribery case and would ultimately help protect BSGR’s assets.

George Soros.

OCCRP found that the case was funded by Mionis. The lawsuit stated that Soros had sabotaged BSGR’s Guinean mining business through “fraud, illegality, defamation, and criminal misconduct.” BSGR demanded at least $20 billion in damages.

The case attempted to place the blame for BSGR’s troubles entirely on Soros, despite copious evidence that BSGR did engage in bribery, as would later be determined by two tribunals and by Steinmetz’s conviction in Switzerland.

Mionis financed the case via Litigation Solutions Ltd., a Bermuda-registered vehicle that he had set up the previous year, court papers reveal. Mionis told OCCRP he had set up the company “in my personal capacity…for the purpose of funding the Soros litigation,” and that he learned about the possibility of financing the case from David Barnett, an in-house lawyer for Steinmetz. Litigation Solutions signed a funding agreement for the case with BSGR in November 2017.

“My decision to invest in this litigation was entirely based on what I understood to be the merits and had nothing to do with my view on Soros personally,” Mionis added.

According to Cramer, in return for $15 million in funding, the company was promised half of the eventual winnings of the lawsuit. Mionis’s company was given priority over BSGR’s other creditors in a follow-up contract, according to two other BSGR executives in court affidavits. This meant that, should the case be successful, Litigation Solutions would be paid from the winnings ahead of any other company or individual owed money by BSGR.

Mionis said Litigation Solutions had to enter “a competitive process with other litigation financing firms” before it was selected as the funder of the Soros case, even though it “was the only bidder.”

The Mionis-backed litigation would become crucial months later, when BSGR entered a form of administration that protected assets from potential future creditors, similar to certain bankruptcy measures in the U.S. While protected by the administration, BSGR could avoid liquidation and keep on operating on the basis that the Soros litigation would be successful, and return the company to solvency.

BSGR needed this protection after it lost, in early 2018, a key skirmish in its arbitration case against Guinea.

For four days, forensic experts had gathered in a temporary laboratory in New York to examine contracts that allegedly detailed BSGR and its middlemen’s promises of payments to Mamadie Touré, the wife of Guinea’s late president.

Steinmetz and BSGR argued the contracts were fake, but in their final report, the tribunal-appointed experts concluded there was no evidence of forgery, and that some of the incriminating documents were signed by BSGR executives and their middlemen.

BSGR now risked losing both of its arbitration cases: not just against Guinea, but also versus Vale, given that both centered on the same bribery allegations.

But in March 2018, before either arbitration panel ruled, BSGR claimed it was unable to pay its creditors and secured an “administration order” in the British Crown Dependency of Guernsey, where the company was registered.

Cramer told Bloomberg this was a strategy to protect its assets as it fought court cases linked to the Guinea bribery scandal.

"We're not in liquidation, no one is forcing this upon us," he said at the time. "This is drawing up the drawbridge, filling up the moat, putting some sharks in the moat.”

To avoid being liquidated, and its assets being sold off to repay creditors, BSGR had to show the company could become profitable again. BSGR presented the Mionis-funded court claim against Soros as its trump card, saying that it expected to win billions in the case. The Guernsey court accepted this logic.

In January 2021, the judge in the Soros case ordered that documents be provided to determine “whether the Company [BSGR] bribed representatives or associates of the Guinean Government” to obtain mining rights” and if this precluded BSGR from claiming it was a victim of Soros. And it was around this time that Litigation Solutions ceased its funding of the lawsuit, after having — Mionis said — put $4 million into the case.

“I just got carried away with optimism. It's wrong and I learned a lesson from that, that I should scrutinize things more,” Mionis told OCCRP. “When I felt it had no chance the obvious thing for me was to pull the plug.”

“They tried to find someone else [to fund the case] but they couldn't ... So the case died once I pulled my funding,” he added. The New York court finally dismissed the lawsuit in October 2021.

Steinmetz’s lawyer said his client “was not involved in negotiating the funding agreement” with Litigation Solutions, and blamed the failure of the lawsuit on “the inability of BSGR’s administrators…to resolve funding issues.” He said Steinmetz was “confident” that more evidence of “unlawful interferences” by Soros would have emerged had the case continued.

Michael Vachon, a spokesman for Soros, said Steinmetz’s allegations are all “false claims”, and were dismissed in arbitration and by judges in Steinmetz’s criminal case in Switzerland.

Barnett, the lawyer who acted for Steinmetz and BSGR, did not respond to questions on the matter.

November 2017: Mionis Buys Chicago Skyscraper with Steinmetz-Linked Company

Documents from the U.S. court case between Vale and BSGR revealed that Steinmetz and Mionis had stakes in a piece of prime Chicago real estate: A skyscraper in the commercial heart of the city, known as the Magnificent Mile.

On November 16, 2017, the Mionis company Fine Arts partnered with a Delaware-registered firm to buy the skyscraper at 500 North Michigan Avenue for $86.4 million. Fine Arts bought 43.5 percent, and the majority 56.5 percent stake was acquired by a company called 500 NMA Acquisition Co. LLC, registered in Delaware. 500 NMA was fully owned by another Delaware company, Perfectus Jerta JV LLC.

Delaware is a renowned secrecy jurisdiction, where the ultimate owners of companies can be kept hidden. Mionis’s lawyers told OCCRP that 500 NMA was owned entirely by Israeli property mogul Amir Dayan and his family at the time of purchase. In an interview with OCCRP, Mionis said that Steinmetz appears to have “a joint venture with somebody else” in the property — an apparent reference to the Dayan family — but did not elaborate further.

A lawyer for Dayan said: “Mr. Dayan does not own the property nor does he have any connection to Beny Steinmetz.” Documents related to the property transaction that were disclosed in court proceedings do, however, provide details of his involvement. For example, in one email Steinmetz representative Gregg Blackstock refers to an October 5, 2017 meeting with Dayan to discuss forming the joint venture that would eventually be named Perfectus Jerta. In another email at the time of the property transaction, Blackstock says “Dayan’s sent two wires” transferring tens of millions of dollars.

Reporters found that a Steinmetz company paid over $5 million of the purchase price and owned at least 11.5 percent of Perfectus Jerta, 500 NMA’s parent company, according to records provided by Mionis’s Fine Arts to Vale, and from the Swiss judgment against Steinmetz. Steinmetz did not answer OCCRP’s questions on his own connections to the skyscraper deal.

Perfectus Jerta is linked to Steinmetz in several other ways, including via its directors and its company name:

Perfectus listed Gregg Blackstock, head of mergers and acquisitions at Steinmetz’s BSGR and director of several other Steinmetz companies, as a manager.

Company records and property purchase documents show Blackstock was a representative of 500 NMA alongside Kenneth Henderson, who had acted as the U.S. counsel to Steinmetz's family foundation, Balda, which owned BSGR. Blackstock signed documents on behalf of the majority-buyer of the skyscraper, while Henderson was named as the addressee for all correspondence.

Blackstock and Henderson were also both directors of the Steinmetz companies Tarpley Belnord and its parent company, Tarpley Property Holdings Inc. Both of these companies changed their names, to Perfectus Real Estate Corp. and Perfectus Real Estate Holdings, on the same day, December 12, 2017. Records show that Perfectus Jerta had also changed its name that day, having previously been known as Tarpley Jerta.

“Even assuming that Steinmetz had some interest in Tarpley/Perfectus, the investment would have been remote and indirect,” lawyers for Mionis told OCCRP, after having earlier said Steinmetz had no beneficial interest in the building. “Our clients had no knowledge of (or reason to inquire about) the structure or beneficiaries of entities that were indirectly invested in the Dayan familyʼs investment vehicle, 500 NMA Acquisition Co. LLC.”

Henderson declined to comment. His law firm Bryan Cave Leighton Paisner said both Steinmetz and Tarpley had been clients, but would not comment further. Blackstock did not reply to questions sent by OCCRP. In a New York civil case in December 2021, Perfectus Real Estate Corp. denied that Steinmetz was its owner.

February 2019: GSOL Helps Cement Deal with Guinea

By 2019, Steinmetz and BSGR were juggling the litigation against Soros with cases against Guinea and Vale, while the Israeli businessman was under increased pressure from multiple criminal investigations. Swiss prosecutors had by now questioned him twice over allegations he had relied on bogus contracts to justify corrupt payments as part of the alleged Guinea bribery scheme.

But then in February 2019, a surprise deal saw Guinea agree to withdraw as a plaintiff in the Swiss criminal case and for the arbitration pitting the country against BSGR to be frozen. Steinmetz negotiated the deal himself, with former French President Nicolas Sarkozy playing the role of broker.

Former French President Nicolas Sarkozy meets President Alpha Condé of Guinea in 2019. The two discussed a planned settlement between Guinea and Beny Steinmetz

Under the deal, which was technically only provisional, the Guinean government would receive $50 million from a GSOL subsidiary, Niron Metals Plc., for rights to Zogota, one of the iron ore licenses that had been canceled after Steinmetz’s alleged bribery came to light.

Steinmetz would be one of Niron’s co-investors in Zogota, said a statement from Bobby Morse, Steinmetz’s long-time spokesman. A “BS co. [Beny Steinmetz company]” would take a 10-20 percent stake in the joint venture with Niron, according to a diagram by Steinmetz’s representatives that was later produced as evidence in court. The provisional settlement itself says that Steinmetz — described as “the BSGR advisor” — introduced the Guinean government to Niron.

The agreement was signed by BSGR’s administrators and the Guinean government. Technically, Niron was not a party to it. But the company put out a congratulatory announcement immediately after the provisional settlement was agreed, and then signed a memorandum of understanding with Liberia to export the iron ore through that country.

Steinmetz, through his lawyer, told OCCRP that he “was offered, under arm’s length terms, options in Niron.” But Mionis denied this, telling OCCRP that options were “not offered, not given.”

“Neither Mr Steinmetz nor any companies associated with him have any financial interest or receive any financial benefits from Niron,” GSOL’s lawyers said.

The agreement was provisional and BSGR’s administrators never agreed to its full implementation. However, key elements were soon put into effect, including instructions being sent to Guinea’s lawyers telling them to withdraw from the Swiss criminal case against Steinmetz, according to a July 2019 letter from the country’s attorney general seen by OCCRP.

“We ask you to note that the Republic of Guinea is formally withdrawing as a civil party against the company BSGR and Mr Beny Steinmetz, in the ongoing criminal procedures and this, in conformity with the measures in article 3.2 of the Settlement Term Sheet,” the letter said.

Niron still hasn’t received mining rights over Zogota, and Mionis doubts it will. “It's taken forever and I don't think it's going to happen,” he said. Niron did not pay the $50 million to Guinea, said Camhis.

Representatives of Sarkozy and the Guinean government did not respond to questions from reporters.

Steinmetz’s legal team used the provisional settlement to pressure Geneva’s prosecutors into backing down in their investigation, leaked correspondence shows.

In a letter to the prosecutors, Steinmetz’s lawyer Marc Bonnant said Guinea had decided Steinmetz “has not made or ordered the least corrupt payment to anyone.” Bonnant cited the Niron deal as evidence of Guinea’s change of heart. This was an exaggeration on his part. In fact, the agreement did not include any retraction from Guinea, and said that neither side accepted the "claims or truth of the remarks" of the other. A representative of Bonnant’s law firm said Bonnant would not comment “due to his confidential mandate with his client.”

But the attempts to derail the criminal investigation failed. Geneva prosecutors charged Steinmetz with foreign bribery in August 2019. He was found guilty in January 2021, and sentenced to five years in prison and a $56 million fine. In April 2022, the sentence was reduced on appeal to three years — half in jail, and half suspended. He is now appealing his bribery conviction to Switzerland’s supreme court.

Separately, Israeli authorities settled with Steinmetz in December 2022, under which he agreed to pay $5 million under the country’s anti-money laundering law, Israel’s Office of the State Attorney said in a statement.

Steinmetz continues to fight to keep his fortune, and his freedom.